Introduction

The goal of this paper is to suggest a framework for understanding and evaluating insurance company stable value contracts in qualified plans. In order to do so, it will focus on the following areas:

- assess the returns on insurance company stable value contracts versus returns on stable value contracts generally, and returns available on money market funds;

- discuss key areas of differentiation among the different types of insurance company stable value contracts;

- explain how the different contract types differ with respect to the extent of required ERISA disclosures and of plan fiduciary responsibilities; and

- suggest appropriate comparisons to non-insurance company stable value contracts.

This discussion will focus on the risk/return, investment and ERISA characteristics of insurance company stable value contracts, not specific contract terms.

Insurance Company Stable Value Returns

Stable value return data is not as available as, for example, returns on money market funds. This makes assessing returns for the asset class as a whole a challenge. Needless to say, assessing the returns for a subset of the asset class presents its own difficulties.

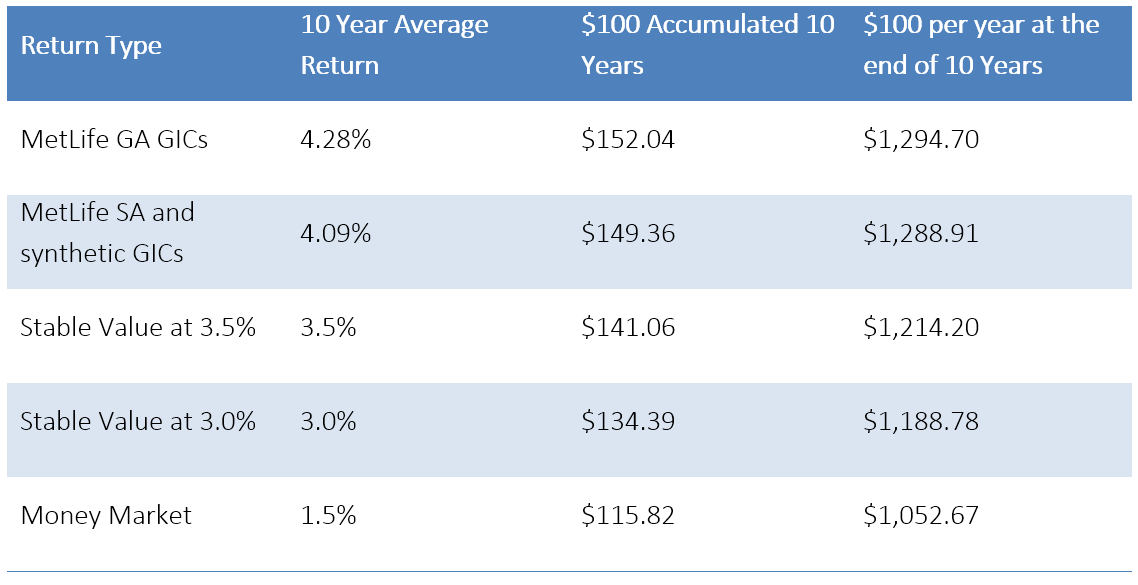

For that reason, the following analysis is based on the results for my own company, MetLife, which, as it has a significant share of the overall insurance company stable value market, may be viewed as providing a representative example of returns available in insurance company contracts. The geometric average for the 10 years ending December 31, 2013 [1] for MetLife general account Guaranteed Interest Contracts (“GICs”) was 4.28% and for MetLife separate account GICs and synthetic GICS combined was 4.09%.[2] This compared to an average net return for stable value funds of between 3.1% and 3.5%.[3] The iMoneynet average taxable money market return for that period was 1.5%.

The table below shows the accumulation of $100 for 10 years, and the accumulation of $100 per year for ten years for MetLife general account GICs, MetLife separate account and synthetic GICs, a stable value return of 3.5%, a stable value return of 3.0% and a money market return of 1.5%.

The data in the table serves as the basis for observations in the balance of this article.

The Insurance Company Regulatory Environment

In the United States, insurance companies are primarily regulated by the individual state insurance commissions. The goal of this regulation is: “to protect the interests of the policyholder and those who rely on the insurance coverage provided to the policyholder.”[4] Insurance regulators aimed at “financial stability” long before the Great Recession of 2008 and the subsequent enactment of Dodd-Frank.

In the event of an insurer’s insolvency, the rehabilitation of the insurer is governed by state law, not by the federal bankruptcy code.[5] State law universally provides more favorable treatment for claims against an insurer by policyholders than it does for other unsecured claims.[[6]] It is worth noting that this differs from other types of financial services firms as well as commercial enterprises generally, where the claims of customers are not placed above those of shareholders, investors or vendors.

Types of Insurance Company Stable Value Contracts

We shall discuss the following types of insurance company stable value contracts: general account guaranteed interest contracts, general account wrap contracts, separate account participating stable value contracts, and separate account non-participating separate account contracts.[7]

The universal element of insurance company stable value contracts is ironically one of the least often discussed: they are insurance contracts. Moreover, they are all group annuity contracts under state insurance law. As noted above, insurance companies have a state, solvency-based regulatory regime that differs from that of virtually all other financial institutions. In particular, state law determines payment priorities in the event of an insurance company’s insolvency. The nature of the contracts as insurance provides valuable protection under most state insolvency regimes. Further, in many jurisdictions, some protection for stable value contracts is available from state guaranty associations.[8]

An important difference between separate account participating stable value contracts and the other types is that the investment assets underlying those contracts are, for ERISA plan investors, ERISA plan assets.

Distinction between “Spread” and “Fees”

One of the most important – and most widely misunderstood – concepts in the stable value arena is the distinction between fees and spreads,[9] and which applies to each type of contract. The fee disclosures required by regulations under ERISA sections 408(b)(2) and 404(a)(5) make it important to distinguish clearly between the two.

Spread

The difference between what the issuer of a debt instrument earns on the funds it has borrowed and the yield the buyer of the debt instrument receives is “spread.” The buyer of an insurance company guaranteed interest contract has no more reason to be concerned about spread than the buyer of a bond: what concerns the buyer is the risk return characteristics of the yield the debt issuer is offering.

Fees and Required Disclosures

“Fees” are deducted from investment earnings and reduce the earnings credited to participants. ERISA 408(b)(2) requires the disclosure of fees assessed against the investment earnings of plan assets to the plan for two reasons: (1) to enable the investor to reduce the yield it can anticipate from market returns by the fees charged, and (2) to enable the sponsor to determine if the fees assessed for the investment management style are reasonable. ERISA 404(a)(5) requires disclosure of fees to participants.

Spreads and Disclosure

There is no comparable requirement for the disclosure of spread for a contract offering a fixed return, because the assets supporting the debt instrument are not plan assets, and the investment performance of the supporting assets does not affect the yield the issuer has guaranteed to the purchaser. Moreover, the yield is known at the point of the investment or allocation decision, and can be easily compared by the sponsor to other similar arrangements in determining which is best for its plan. The Department of Labor recognized this important distinction for insurance products used in ERISA funds.[10]

Spread is in any case an estimate. The issuer of a debt instrument has no doubt priced for some anticipated spread, but whether or not that spread will be achieved is dependent on the performance of the investment in which the issuer has invested the debt proceeds.

404(a)(5) Example

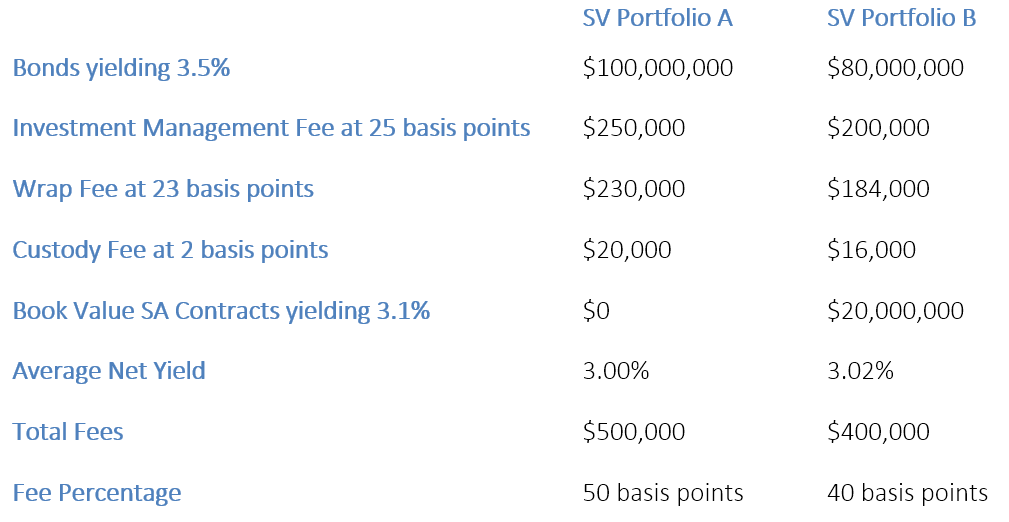

For stable value investments, plans must report to participants: (1) the amount and a description of each fee charged directly against a participant’s investment and (2) the total annual operating expenses of the investment expressed as a percentage, among other things not figuring in our example. (29 CFR 2550.404a-5(d)(iv)(A)&(B)).

For illustration, let’s see how this works for the following two stable value investment portfolios of the same size and with approximately equal yields. This example assumes direct management by the plan without sponsor asset-based charges. If there was a stable value manager with an asset based charge, and/or plan sponsor charges assessed against participant account balances, the total fees illustrated would rise by the same amount for both portfolios.

For the bonds, the investment management fee, the wrap fee and the custody fee are charged against the value of the assets, and must be disclosed. The insurance company has no doubt made provision for its expenses in determining the guaranteed rate it would offer on its book value separate account stable value contract, but, depending on the performance of the assets in which the company invested the funds it received from the plan, the company may or may not actually recover its expenses. Further, under the definition of plan assets, assets supporting guaranteed benefit contracts are not plan assets, another good reason why the cost of managing the assets does not concern the plan sponsor or participants. The result is that a reallocation of a part of a managed stable value bond portfolio to insurance company fixed return stable value contracts will certainly reduce the option’s expense ratio and would likely modestly increase rates credited to participants as well.

General Account Guaranteed Interest Contracts

A general account guaranteed interest contract (“GIC”) is a group annuity contract that integrates the benefit responsive guarantee with a promise to pay which is backed by the claims-paying ability of the insurer’s general account. Since the amounts available under the contract are not allocated by the insurance company to individual participant accounts, a GIC is an unallocated group annuity contract.[11] It is similar to an unsecured corporate bond, but with credit characteristics more favorable to the purchaser because of the priorities of the insurance insolvency regime. It has a higher credit quality than an unsecured bond of the same insurance company issuing the GIC because claims under a group annuity contract rank as policyholder claims, and in the event of an insurance company’s insolvency, above the claims of unsecured creditors.[12]

What should a purchaser of a GIC care about? As an ERISA fiduciary, he or she has a duty to diversify and the duty to invest with the skill of a prudent expert. A general account GIC exposes the plan to the claims-paying ability of the insurance issuer for the amount of the GIC.[13] Most plan sponsors and stable value managers will limit the exposure to the general account of any issuer, with the limit determined by the rating of the issuer’s claims paying ability[14] and the GIC’s maturity date. Since security of principal is the cornerstone of stable value, a minimum issuer claims paying ability rating is likely to be another requirement.

As a GIC integrates the benefit responsive guarantee with the underlying investment, the most appropriate comparison for risk/return evaluation is not to a bond, but to a wrapped bond. That is, it is appropriate to compare the yield on a general account GIC to the expected yield of a comparable bond less the cost of a synthetic wrap to provide the benefit responsive guarantee for that bond.

Participating versus Non-Participating

The comparison should not stop with the synthetic wrapped bond yield to GIC yield. Synthetic wraps currently available in the stable value market are “participating” wraps. The crediting rate on a bond with a synthetic wrap is affected by the interplay between changes in market interest rates and participant withdrawals. If participants withdraw funds covered by a synthetic wrap contract when interest rates have risen and the value of the underlying bonds has fallen, that will depress the yield on the remaining participant balances below the original level.[15] By contrast, changes in market interest rates and withdrawals do not affect the rate credited on a GIC. The rate credited on the remaining participant balances is the same as that which was credited on the unreduced balance. This is a very important distinction, depending on a plan fiduciary’s or stable value manager’s view on cash flows and interest rate movements. When the yield on a GIC exceeds that of a wrapped bond of comparable credit quality, a rational manager could well conclude that the plan was obtaining valuable additional protection.

Status Under ERISA

In an advisory opinion, the Department of Labor advised:

Under section 401(b) of ERISA, if an insurance company issues a “guaranteed benefit policy” to a plan, the assets of the plan are deemed to include the policy, but do not, solely by reason of the issuance of the policy, include any assets of the insurer. However, in its decision in John Hancock Mutual Life Insurance Co. v. Harris Trust & Savings Bank, 510 U.S. 86 (1993) (Harris Trust), the Supreme Court interpreted the meaning of “guaranteed benefit policy,” as defined in ERISA section 401(b)(2)(B), and held that a contract qualifies as a guaranteed benefit policy only to the extent that it allocates investment risk to the insurer. Under the reasoning of this decision, an insurer’s general account would be treated as holding plan assets to the extent it contains funds which are attributable to any non-guaranteed components of contracts with employee benefit plans.[16]

As all GIC assets are guaranteed, the general account does not contain ERISA plan assets due to the sale/purchase of a GIC.

Comments on Returns

The table shows that MetLife GIC returns exceed those for MetLife SA and synthetic GICs by 19 basis points, and exceed the yield of our top of range estimate for stable value generally by 78 basis points. In the context of the conservative fixed income space, 19 basis points are substantial, and 78 may be viewed as conclusive. What is a stable value manager gaining who forgoes that premium? The active manager is foregoing the possibility of a capital gain on a future trade, and if a manager can demonstrate a record of such gains, then for purposes of comparisons the yield of a freely traded bond should be increased by the manager’s historical capital gain alpha. However, even for active managers where an adjustment for expected alpha is justified, it is highly unlikely that the capital gains component approaches 19 basis points, or 78 basis points.

An adjustment for option liquidity is not justified for any stable value contract, including GA GICs. As noted above, all stable value contracts must provide liquidity at contract value for uncoordinated participant transactions.

Book Value Separate Account Contracts

Book value separate account[17] (BVSA) stable value structures combine the diversification benefits of a separate account contract with the certainty of a guaranteed interest contract.

29 USC §1104(a)(1) makes diversification one of the primary responsibilities of an ERISA fiduciary. The fiduciary discharges his duties in part by: “diversifying the investments of the plan so as to minimize the risk of large losses, unless under the circumstances it is clearly prudent not to do so.” Many plan sponsors and stable value investment managers have interpreted their diversification fiduciary duty in investment policy statements and guidelines that limit the maximum exposure to a single credit, like that of an insurance company general account.[18]

State insurance law allows insurance companies to establish accounts legally distinguished in insolvency proceedings from the general account. Those accounts are called “separate accounts,” and owners of separate account contracts have first claim on the assets of the separate account, to the extent of their claim under the contract. This means that if the contractholder is owed $100 under the contract, and the separate account has $102 in assets, a contractholder with a market value right of exit would get $102 and if all participants as a group withdrew their stable value balances, they would collectively receive $100.

Separate accounts which back insurance company contracts hold a diversified pool of assets, and cannot hold any obligations of the insurer. Book value separate accounts are governed by the same state law investment restrictions that apply to the general account.

In the case of a book value separate account stable value contract, a plan has no exposure at all to the insurer’s general account unless the book value of the separate account is less than the contract’s value. When the separate account value is lower, the plan has an exposure in the event of the insurer’s insolvency to the excess of contract value over separate account value. For example, a plan fiduciary conservatively evaluates the exposure to the issuer of a book value contract as 5% of the initial deposit. That means that the plan fiduciary could buy 20 times as much of the book value contract consistent with its diversification limits as it could of a general account product of the same issuer.

Non-Participating

Like the GIC, the book value separate account product does not participate in the investment experience of the insurer or in the withdrawal experience of the plan. The original guaranteed rate continues despite the timing or amount of participant withdrawals. Thus, also like the GIC, plan fiduciaries prudently compare the returns on these contracts to the yield of a bond less the charge for wrapping the bond, and less any added value the fiduciary attributes to a non-participating wrap.

Status under ERISA

28 CFR 2510.3-101(h)(1)(iii) provides, in relevant part:

When a plan acquires or holds an interest in any of the following entities its assets include its investment and an undivided interest in each of the underlying assets of the entity: …A separate account of an insurance company, other than a separate account that is maintained solely in connection with fixed contractual obligations of the insurance company under which the amounts payable, or credited, to the plan and to any participant or beneficiary of the plan (including an annuitant) are not affected in any manner by the investment performance of the separate account.

The investment performance of a book value separate account has no effect on the interest rate credited under the contract. Therefore, the assets of the separate account are not plan assets. Parallel to a GIC and the general account, for a book value separate account neither the plan sponsor nor the issuing insurer is an ERISA fiduciary with respect to the underlying assets. The plan fiduciary is acting in its fiduciary capacity when it chooses to purchase the book value separate account group annuity contract. Thus, the appropriate comparison with respect to performance of the book value separate account stable value contract is the yield on an otherwise similar bond, less the cost of wrapping a bond, with an adjustment for the value of non-participation. The availability of the insulated separate account would encourage a larger allocation to a book value separate account product than to a GIC of the same issuer.

Participating Separate Account Contracts

In a participating separate account stable value contract, all the investment performance of the separate account flows immediately to the plan and over time to the accounts of participants, though the operation of the contract’s crediting rate formula. Stable value rates credited in MetLife’s participating insurance company contracts have generally exceeded those for stable value overall, which have in turn exceeded those for intermediate bond funds.[19] Thus, unlike the other insurance company contracts, both the insurer and plan sponsor have fiduciary responsibility with respect to the management of the underlying assets.

Further, participant withdrawals also affect the crediting rate in the standard participating separate account contract. Participant withdrawals when the market to book ratio is below one reduce the crediting rate, and participant withdrawals when the market to book ratio is above one increase the crediting rate.

Regulations under Section 408(b)(2) require complete disclosure of all fees charged with respect to the management of the plan assets. The plan sponsor as a fiduciary must take into account not only issuer credit and reasonability of the fees charged, but also the separate account investment options available, and the ability of the insurance company to discharge its fiduciary duties with respect to direct investment management or monitoring of subadvisors retained to provide direct investment management of the separate account assets.

Synthetic GICs

Insurers also issue “synthetic” GIC contracts. The operation of a synthetic GIC is parallel to that to that of a separate account GIC, but title to the wrapped asset portfolio is held directly by the plan, not by the insurance company issuing the synthetic GIC. From the plan’s perspective, direct title may reduce the plan’s exposure to operational issues potentially arising from an insurer’s insolvency. For a synthetic GIC, a plan sponsor might conclude that higher issuer limits were prudent than for a general account or even for a separate account stable value contract.[20]

Conclusion

Insurance companies have been an enduring presence in the stable value contract market, but that has not meant that insurance company stable value contracts are well – or consistently – understood.

Once stable value structure is understood, it is not difficult to compare products between stable value as well as other fixed income investments.

Fair comparison requires recognition not only of historical returns, where there is meaningful evidence of insurance contract outperformance, but also of an array of contract characteristics: the nature of the support for the contract liabilities, whether or not underlying assets supporting liabilities are plan assets, state insurance insolvency priorities and guaranty coverage, and potential differences in value between participating and non-participating contracts.

It is my hope that this article will assist plan sponsors and those who advise them in identifying and making appropriate value distinctions that will enable stable value to best serve their plans and their participants.

[1] The average is based on actual data for 2005 through 2013, and an estimate for 2004 that assumes a somewhat larger rate reduction compared to 2005 than that experienced for the stable value funds for which I have ten years of MetLife data.

[2] The returns aggregate all general account GICs, regardless of duration, and all separate account GICs and synthetic GICs, regardless of duration of the underlying portfolios. The returns are net of all MetLife fees, including those for management of the assets of the separate account, but could be greater than those credited to participants because of the deduction of the fees of a stable value manager or pooled fund. The amount by which MetLife returns exceed those for stable value generally indicates that the durations of the MetLife wrapped portfolios are longer than the stable value average. This is largely due to the limited exposure in MetLife stable value contracts to cash exits from stable value pooled funds at contract value even when it exceeds market value. Some collective investment funds invested in MetLife contracts require participating plans to exit at the lower of contract value or market value. While potentially inconvenient for a plan sponsor that wishes to make a change, this provision eliminates any issuer risk of a collective investment fund death spiral, and thereby makes longer durations, with their expected higher returns, safer for the issuer as well as the plans and plan participants that remain in the fund. These funds have returns as reported by Morningstar at or near the top for each and every historical period reported as of 12/31/2013. While the plan sponsor/fiduciary may accept exit provisions that limit payouts to the lesser of contract value or market when exiting the fund, the plan sponsor/fiduciary generally gains a higher returning stable value fund for the plan and its participants.

[3] Morningstar data for collective investment funds net returns shows a ten year arithmetic average return (of the geometric average for each fund) of 3.2%. A different Morningstar data base of such funds shows an average return of 3.05% and a twentieth percentile return of 3.59%.

[4] http://www.naic.org/documents/committees_e_us_solvency_framework.pdf. The NAIC refers to this system as a “risk-based solvency system.” http://www.naic.org/cipr_topics/topic_global_regulatory_convergence.htm, and state insurance regulation is frequently described as “solvency-based.”

[5] In New York, e.g., insurer insolvencies are governed by Article 74 of the Insurance Code.

[6] See, e.g., New York State Insurance Code §7435.

[7] The contract types we have labelled “separate account” can be described as “separate account supported, but with general account guarantees.” A contract supported by the value of the assets of a separate account could not meet the requirements of AAG INV-1 (SOP 94-4-1) (FASB Staff Position, issued December 29, 2005) that stable value contracts support all participant withdrawal and transfer activity at contract value.

[8] This article will use the New York regulatory regime that applies to Metropolitan Life Insurance Company as its principal example of state regulation. For a New York contract holder, unallocated group annuity contracts and funding agreements have guarantee coverage up to a maximum of $1,000,000. §7708(a)(3)(ii).

[9] This section is adapted from my article The Distinction between “Spread” and “Fees” in Stable Value Insurance Contracts, 64 RISKS AND REWARDS 8 (Investment Section of the Society of Actuaries, August, 2014).

[10] Federal Register, Volume 75, Number 202, “Department of Labor, Employee Benefits Security Administration 29 CFR Part 2550, Fiduciary Requirements for Disclosure in Participant-Directed Individual Account Plans; Final,” PAGE 64916.

[11] Although in a defined contribution plan option, the sum of the participant account values must equal the total for the option, the plan level entitlement does not translate into individual entitlements at the level of the contracts that fund the option. This distinction is important in determining the amount of state guaranty association coverage, if any, that might be available to a plan in the event of the failure of an issuer of a group annuity contract to honor the contract claims.

[12] See §7435 of New York State Insurance Law. The conclusions about the operation of New York law are not legal advice. Interested readers should consult their own counsel for legal advice about the matters discussed in this paper.

[13] This may not be true where state guaranty association coverage is available, and the prudent fiduciary will take guaranty coverage into account when evaluating a financial instrument, as IRS IB 95-1 makes clear.

[14] There are two primary types of ratings with regard to insurance companies. First is a rating agency’s opinion of an insurer’s financial strength and ability to meet its financial obligations to policyholders. Second is a rating agency’s opinion of the creditworthiness of specific corporate securities and the issuer’s ability and willingness to meet those obligations when due. The ratings provide the public, as well as institutions, with a tool to gauge an insurer’s ability to meet its ongoing obligations to policyholders (i.e., “financial strength ratings”) and the ability to fulfill certain debt obligations, for instance, on securities issued (i.e., “issuer credit ratings”).

[15] Of course, the opposite is also true, but as an investment option in defined contribution plans whose primary role is safety rather than yield, the former is the more important observation.

[16] See http://www.dol.gov/ebsa/regs/aos/ao2005-19a.html.

[17] “Book value” in this context means a separate account that supports contracts, but where the rate credited on the contract does not depend on the investment performance of the separate account. It is an insurance department regulatory concept, not a synonym for participant contract account balances.

[18] As we shall discuss below, participating separate account contracts generally invest in a pool of fixed income assets of intermediate duration.

[19] See https://www.stablevalue.org/knowledge/faqs/question/how-does-stable-value-compare-to-other-investment-options.

[20] This is not to suggest that holding the assets directly is without risk to the plan. As the plan will have contracted separately for asset management, it will bear responsibility for the risks associated with manager oversight, valuation risk, inappropriate trading and similar matters.