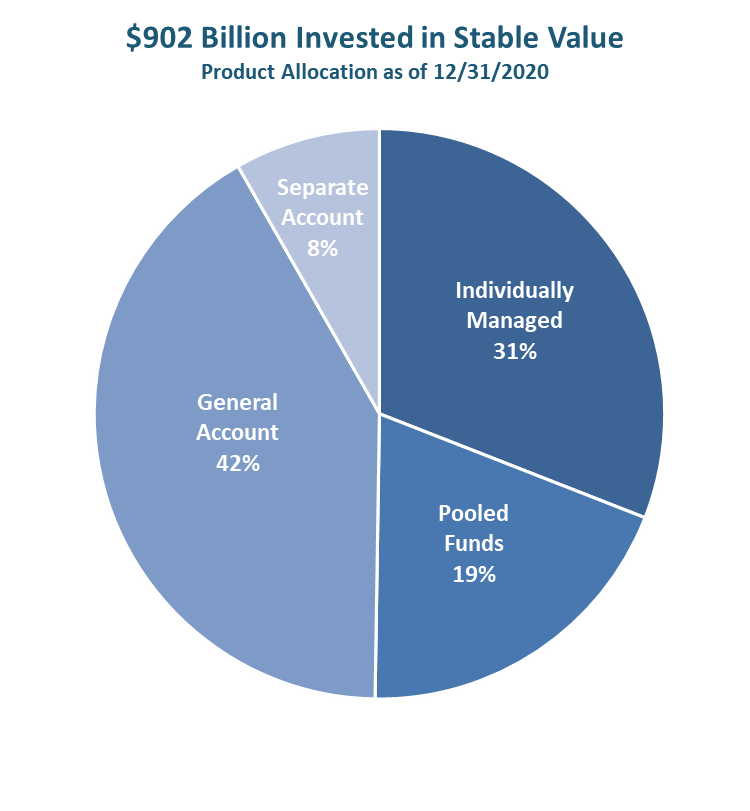

Given the complexity and uncertainty of today’s financial markets and economy, it is no wonder that plan sponsors and participants continue to appreciate the benefits of stable value. As of December 31, 2020, more than 185,000 defined contribution plans invested $902 billion in stable value products.[i] Throughout its 45 year history, stable value has consistently delivered a unique combination of benefits: liquidity, principal preservation, and consistent, positive returns.

Stable value funds are tailored to meet the needs of a specific plan participant population and/ or group of plans and their plan participants. While all stable value funds have weathered various economic cycles and consistently performed in meeting the needs of plan participants, there are differences in structure, levels of guarantees, as well as some contractual features. Because of the significant allocation of assets to guaranteed insurance accounts and the scant amount of publicly available information, the following frequently asked questions (FAQ) seeks to shed some light on this segment. This FAQ is limited to an overview of guaranteed insurance accounts and focuses primarily on ‘spread-based’ general account insurance products. The FAQ does not address all the variations of guaranteed insurance accounts or the combination of stable value funds that may be used by a plan. This FAQ also does not discuss or compare other stable value segments such as individually managed or pooled funds or differences in investment management.[ii]

[i] SVIA 2020 Annual Investment & Policy Report

[ii] For more information about stable value segments other than guaranteed insurance accounts, please see www.stablevalue.org.